Sweepstakes vs Social vs Real Money Casinos: Key Differences

Three distinct types of online casino operate in the United States simultaneously, and most players couldn’t tell you the structural differences between them. Social casinos, sweepstakes casinos, and real-money iGaming platforms all offer slots, table games, and digital entertainment — but their legal foundations, revenue models, payout structures, and player protections are fundamentally different. Choosing between them isn’t just a matter of preference; it’s a decision shaped by your state of residence, your risk tolerance, and whether you care about regulatory oversight.

This casino model comparison uses data from the American Gaming Association, KPMG, Eilers & Krejcik Gaming, and other industry sources to map the three models across the dimensions that matter most: how they make money, how much they return to players, where they’re legal, and what protections exist when something goes wrong. The goal isn’t to advocate for one model over another — it’s to give you enough information to understand what you’re actually using when you open any of these platforms.

The differences are larger than most people assume. A social casino and a sweepstakes casino can look identical on screen while operating under completely different legal and economic frameworks. Understanding those frameworks is the first step toward making an informed choice about where — and how — you play.

The Social Casino Model: Playing Without Real Money Prizes

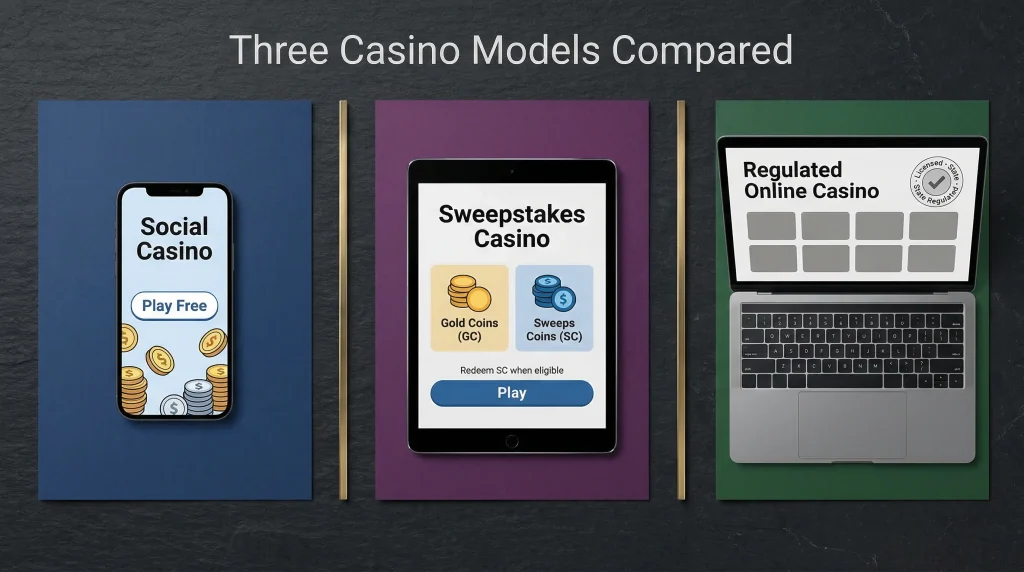

Social casinos are the simplest of the three models: you play casino-style games with virtual currency, and that currency never converts into real money. There’s no redemption path, no prizes, no cash-out. The coins you earn and spend exist entirely within the platform, and when your balance hits zero, you either wait for a free refill or purchase more virtual coins. The entertainment is the product. Full stop.

The category includes some of the most downloaded gaming apps in the world. Titles like Slotomania, Big Fish Casino, Heart of Vegas, and DoubleDown Casino have dominated app store rankings for over a decade, generating revenue through in-app purchases of virtual coin packages. The economics are straightforward: players buy virtual currency, they play until it’s gone, and the developer keeps everything. There are no payouts, no prizes, and no regulatory friction.

The scale of this market is often underappreciated. According to data cited by the Social and Promotional Gaming Association, drawing on Eilers & Krejcik Gaming research, Americans have spent more than $40 billion on social casino virtual currency over the past decade. That’s $40 billion with no possibility of winning anything back — a revenue stream built entirely on entertainment value and the psychological engagement loops that keep players spinning.

Legally, social casinos face almost no regulatory hurdles. Because there’s no real-money prize component, the gambling-law tripod (consideration, chance, prize) is missing two legs: the “prize” element is virtual, and the “consideration” argument is weakened because the purchase is for entertainment, not a chance at money. Social casinos are available in all 50 states, require no gambling license, and are subject to the same regulations as any other mobile game or entertainment app.

The player protection landscape reflects this hands-off status. Social casinos have no obligation to disclose RTP, publish payout data, or provide responsible gambling tools. Some developers have voluntarily implemented spending limits and cool-down features, but adoption is inconsistent. The consumer protection framework for a social casino player is essentially the same as for anyone buying coins in Candy Crush — general consumer law, not gambling regulation.

For players, the value proposition is pure entertainment. If you enjoy casino-game mechanics — the lights, the sounds, the dopamine hit of a winning combination — and have no interest in real-money outcomes, social casinos deliver that experience cleanly. The trade-off is clear: you’re paying for fun, and the fun is all you’re getting.

The Sweepstakes Casino Model

Sweepstakes casinos occupy the middle ground — and the contested ground — between social casinos and regulated iGaming. The games look the same as social casinos, the interface is nearly identical, but one structural addition changes everything: a second currency that can be redeemed for real prizes.

The dual-currency system works like this. Gold Coins are the entertainment currency — purchased, played with, but never redeemable. Sweeps Coins are the promotional currency — received as free bonuses alongside GC purchases (or through daily logins, AMOE, and other free entry methods) and convertible into cash prizes after meeting playthrough requirements. The legal argument is that players purchase entertainment (Gold Coins) and receive sweepstakes entries (Sweeps Coins) as a free promotional bonus, meaning no “consideration” is required for the prize-eligible portion of the experience.

The market has grown at a pace that caught the regulated industry off guard. KPMG’s sweepstakes gaming primer reports that the social casino sector — which includes sweepstakes platforms — reached approximately $7.1 billion in gross gaming revenue in 2026, with the sweepstakes segment growing at a compound annual rate of 60% to 70% between 2020 and 2026. That growth rate puts it among the fastest-expanding segments in the broader gaming industry.

The legal status is the model’s defining tension. Sweepstakes casinos operated in 40-plus states as recently as 2026. By early 2026, six states have enacted bans, and more legislation is pending. The platforms argue they’re promotional sweepstakes, not gambling. State legislators and the regulated gaming industry argue the opposite. The outcome of this debate will determine whether the sweepstakes model survives in its current form, evolves into a regulated framework, or gets legislated out of existence in key markets.

The economics of the sweepstakes model sit between its two neighbors. Social casinos retain 100% of revenue because there are no prizes. Regulated casinos retain only 3–5% per wager because of competitive RTPs and regulatory floors. Sweepstakes casinos retain approximately 30–35% of Gold Coin sales after returning 65–70% to players as SC prizes. That retention rate — far higher than regulated gambling but lower than pure entertainment products — reflects the model’s dual nature: part entertainment platform, part prize system, structured to generate substantially more operator revenue per dollar of player spending than a licensed casino would be permitted to retain.

The competitive challenge for sweepstakes operators is that the closer their product resembles real gambling — and AGA research shows that 90% of their own players perceive it as gambling — the harder it becomes to defend the promotional classification that keeps them outside regulatory frameworks. Every improvement in game quality, every expansion of the game library, every new player who joins specifically to win money pushes the product further from “promotional sweepstakes” and closer to “unlicensed online casino” in the eyes of legislators.

The Real-Money iGaming Model

Real-money iGaming is what most people picture when they think of an online casino: you deposit real dollars, wager on slots and table games, and withdraw your winnings directly to your bank account. There’s no dual currency, no promotional framing, and no ambiguity about whether the activity is gambling. It is, explicitly, and it’s regulated accordingly.

The catch is access. As of 2026, legal online casino gambling is available in only about seven states: New Jersey, Pennsylvania, Michigan, West Virginia, Connecticut, Delaware, and Rhode Island. Each state requires operators to obtain a license, submit to regulatory audits, maintain certified RNG systems, and comply with player protection mandates. The barriers to entry are high — and deliberately so. Licensing fees, compliance costs, and ongoing regulatory obligations mean that only well-capitalized, legally vetted companies can operate.

The scale of the regulated market provides important context. The AGA’s Commercial Gaming Revenue Tracker reports that U.S. commercial gaming generated $78.72 billion in gross gaming revenue in 2026, a 9.2% year-over-year increase. Within that total, iGaming crossed $1.03 billion in monthly revenue for the first time in December 2026, a 22.4% increase from the prior year. Those figures represent the economic weight of the regulated market — and the revenue base that the traditional industry is defending against sweepstakes encroachment.

For players, the iGaming model offers the strongest consumer protections available. RTPs are audited by independent testing labs like eCOGRA, GLI, and BMM Testlabs. Dispute resolution goes through state gaming commissions with real enforcement authority. Payout ratios are publicly disclosed. Self-exclusion lists are maintained at the state level, and problem gambling resources are mandated, not optional. When something goes wrong — a delayed payout, a disputed game outcome, a suspected RNG issue — there’s a regulatory body with the power and obligation to investigate. This oversight infrastructure doesn’t exist at social or sweepstakes casinos, and it’s the primary reason that consumer protection advocates prefer the regulated model despite its limited geographic reach.

The payout experience reflects the regulatory difference. At a licensed iGaming site, withdrawals typically process within 24 to 72 hours, and the methods available include bank transfer, e-wallets, and in some cases cryptocurrency. There’s no playthrough requirement on deposited funds (though bonus funds may carry conditions), and the path from win to bank account is direct and transparent. Compare that to the sweepstakes model’s multi-step process — playthrough, minimum thresholds, KYC at first redemption, 3-to-7-day processing — and the operational advantages of regulation become clear.

The trade-off is geographic exclusion. The vast majority of Americans live in states where legal online casino gambling simply isn’t available. That access gap is the primary reason sweepstakes casinos exist — they fill a demand that the regulated market can’t serve because state legislatures haven’t opened the door. Whether filling that gap through an unregulated promotional model is better or worse than having no option at all is the fundamental policy question driving the current legislative debates.

Side-by-Side Comparison

| Category | Social Casino | Sweepstakes Casino | Real-Money iGaming |

|---|---|---|---|

| Legal Classification | Entertainment/gaming app | Promotional sweepstakes | Licensed gambling |

| State Availability | All 50 states | 40+ states (shrinking) | ~7 states |

| Real-Money Prizes | No | Yes (via SC redemption) | Yes (direct withdrawal) |

| Regulatory Oversight | None (consumer law only) | None (self-regulation) | State gaming commission |

| RTP Auditing | Not required | Not required | Mandatory (independent labs) |

| Player Payout Ratio | 0% (no cash prizes) | 65–70% (aggregate) | ~95–97% (game-level RTP) |

| Revenue Model | In-app purchases | GC package sales | House edge on wagers |

The table reveals the core structural differences, but the numbers behind each model tell a more nuanced story.

On payout ratios, the gap between sweepstakes (65–70% system-level) and iGaming (95–97% game-level) is the single biggest differentiator for players who care about real-money outcomes. A sweepstakes casino retains roughly 30–35 cents of every dollar that enters the system. A regulated online casino retains 3–5 cents per dollar wagered. These numbers aren’t directly comparable — one measures purchase-to-prize conversion, the other measures wager-to-return — but the directional difference is stark. Players at regulated casinos get significantly more of their money back per unit of activity.

On advertising, the competitive pressure between models is intense. AGA research using Sensor Tower data found that sweepstakes casino advertising accounted for approximately 50% of all online casino ad impressions in early 2026. That means half the digital casino advertising reaching American consumers promotes platforms operating outside state gambling regulation. For the regulated industry, this isn’t just a revenue threat — it’s a consumer confusion problem, because players often can’t distinguish between ads for licensed operators and ads for unregulated sweepstakes platforms.

Tres York, VP of Government Relations at the AGA, characterized the sweepstakes sector’s positioning this way: these operators “present themselves like legal, regulated platforms — but they operate outside the law and regulation.” That framing reflects the regulated industry’s core concern — not just competition for revenue, but the erosion of consumer trust in a marketplace where regulated and unregulated products look identical.

On responsible gambling, the divergence is equally significant. Regulated iGaming operators are required to implement self-exclusion programs, contribute to problem gambling funds, and comply with advertising restrictions. Social casinos and sweepstakes casinos have no comparable mandates. Some do offer voluntary tools — VGW’s platforms include basic self-exclusion options, for instance — but the depth and enforcement of those tools don’t match what state regulation requires. For players concerned about gambling harm, the regulatory protections available at iGaming sites simply don’t exist at social or sweepstakes platforms.

Which Model Fits Your State

Your available options depend first on geography, second on what you want from the experience.

If you’re in one of the roughly seven states with legal iGaming — New Jersey, Pennsylvania, Michigan, West Virginia, Connecticut, Delaware, or Rhode Island — you have access to all three models. The practical recommendation is straightforward: for real-money play, use a licensed iGaming platform. The consumer protections, audited RTPs, and regulatory oversight make it the clearly superior option when real money is on the line. Social casinos and sweepstakes casinos still serve a purpose in these states — social for zero-stakes entertainment, sweepstakes for a different game selection or promotional bonuses — but they shouldn’t be your primary real-money venue when a regulated alternative exists.

If you’re in one of the 40-plus states where sweepstakes casinos are legal but iGaming is not, the choice is between social casinos and sweepstakes platforms. Here, your goals matter. If you want pure entertainment with no financial component, a social casino delivers that cleanly. If you want the possibility of winning real prizes and you’re comfortable with the reduced consumer protections, a sweepstakes casino fills the gap left by the absence of regulated iGaming in your state.

If you’re in a state that has banned sweepstakes casinos — California, New York, Connecticut, Montana, New Jersey, or Nevada — your legal options for online casino-style gaming are limited to social casinos (everywhere) or regulated iGaming (where available). Accessing a sweepstakes casino from a banned state is a violation of both the platform’s terms of service and potentially state law.

Regardless of your state, one principle applies universally: understand what protections you’re giving up before you play on any platform. The differences between these three models aren’t aesthetic — they’re structural, legal, and financial. Knowing which model you’re using, and what that model does and doesn’t provide, is the minimum level of awareness any player should bring to the experience.

Future Convergence: Will These Models Merge?

The boundary lines between these three models are already blurring. Sweepstakes casinos offer experiences that are functionally identical to regulated online casinos. Social casinos have experimented with reward features that approach (but stop short of) real-money redemption. And the regulated iGaming market continues its slow state-by-state expansion. The question is whether these models will eventually converge into a single, regulated framework — or continue to coexist as distinct legal categories with overlapping products.

The clearest sign of convergence is the emergence of sweepstakes sportsbooks. Platforms like Fliff and Novig have applied the dual-currency model to sports betting, offering Sweeps Coin wagers on real sporting events with prize redemption for correct picks. This extension of the sweepstakes model into a domain that is heavily regulated in licensed states has intensified the regulatory backlash and accelerated the legislative response. If sweepstakes casinos were a gray area, sweepstakes sportsbooks turned the gray darker.

The industry’s own leadership is signaling a desire for formal regulation. Jeff Duncan, Executive Director of the SGLA and a former member of Congress, has been explicit: “We want to be regulated. We want to pay taxes.” That message, delivered at the NCLGS conference in December 2026, represents the sweepstakes industry’s official position — an acknowledgment that self-regulation has limits and that a state-licensed framework, while more costly and restrictive, would provide the legitimacy needed to survive the current legislative environment.

Whether states will choose to regulate rather than ban is the open question. The six bans enacted in 2026 suggest that many state legislatures prefer prohibition. But others — particularly states that lack iGaming infrastructure and see revenue potential in regulated sweepstakes — may opt for a licensing framework that brings the industry under state oversight while capturing tax revenue. The SGLA’s economic analysis for Florida, estimating $63 million in potential tax revenue from a regulated sweepstakes market, illustrates the fiscal argument for regulation over prohibition.

The most likely trajectory is fragmentation: some states will ban, some will regulate, some will continue to ignore the category, and a few will attempt hybrid frameworks that satisfy neither side. For players, this means the “which model fits your state” question will only become more complicated as 2026 unfolds. The models may eventually merge, but that convergence is a multi-year legislative process, not a near-term outcome. In the meantime, the three models will continue to coexist — competing for the same players, offering increasingly similar products, and operating under radically different rules.